How China Paves the New Silk Road

How China Paves the New Silk Road

Or One Belt, One Road; or, Belt and Road Initiative. It's confusing.

So let’s take a quick flashback to 2014ish where we find ourselves on the mean streets of your favorite expat neighborhood in your favorite Asian city. It actually doesn’t matter which expat neighborhood in which city in Asia because the chatter was all the same about what would become the biggest international relations buzzword in Asia since “global governance”: One Belt, One Road.

I never really paid all that much attention to the chatter but it was everywhere. And the gist of it was that China was launching an IMF meets World Bank meets Marshall Plan foreign policy initiative. They were going to build a canal through Thailand to circumvent the Straits of Hormuz, finance mines in Africa to gain access to precious metals and abject poverty, and build a railway through Kazakhstan to disrupt British gap year students. Or whatever. I didn’t really care.

Until last year when I stumbled on this report which got their hands on the actual financial documents used in Chinese lending programs1. So let’s review how this IR buzzword played out in practice:

Where did the money actually go?

So I called up a buddy to get some color on the Africa side of this. Let’s just say he’s a credible person when it comes to geopolitics on the continent. I’ll summarize his reactions:

This map heavily under represents Chinese influence. They’re “everywhere”.

Places like Uganda and Kenya are free agents. It’s pay to play there and the US largely pisses those leaders off by having running commentary on human rights issues. Interesting to see they’re not on the list.

The DRC is the total wild west. There’s tons of minerals but there are unreal creditworthiness issues above and beyond everything else on that map.

Botswana is an interesting one. They’re the “success story in southern Africa” given their political stability. Stable enough that Debeers has their headquarters there.

The "US continues to fuck up their foreign policy by sending their worst diplomats. This is a bipartisan issue. They’re all C-list talent”. I got bad news for you: there’s no such thing as A-list civil servants.

Overall, I think this is an incomplete picture but enough to provide a flavor.

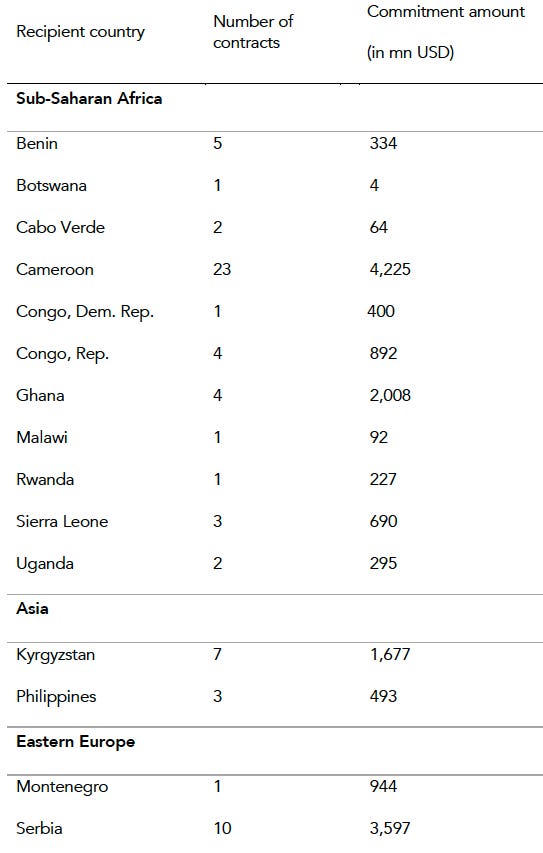

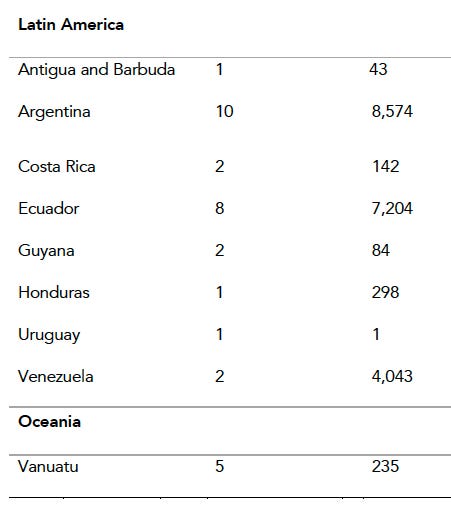

How much was lent?

I wonder what you get for $4bn in Argentina or $8.5bn in Venezuela besides a lot of writedowns.

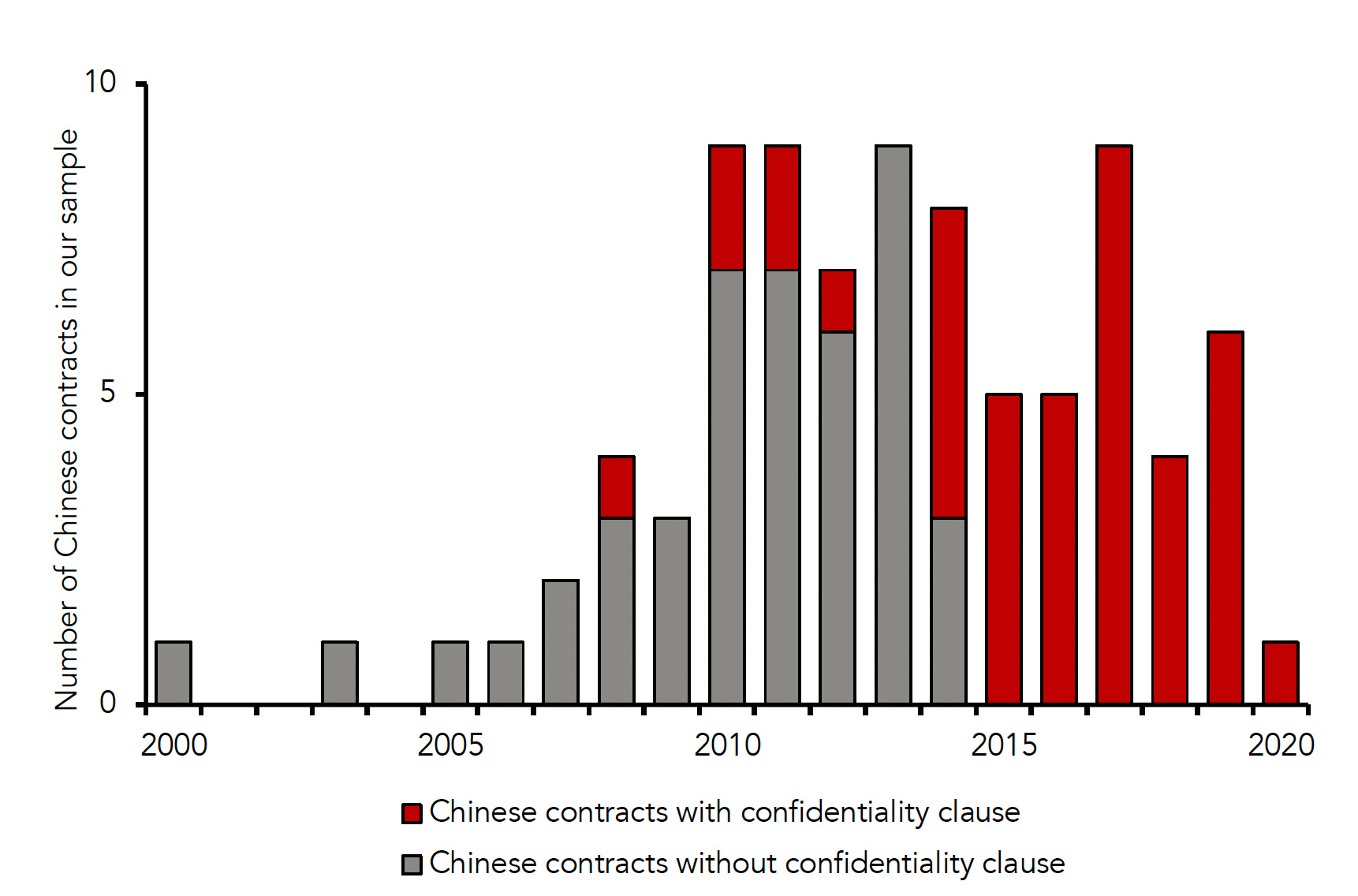

“Unique” Terms

… the Chinese contracts contain unusual confidentiality clauses that bar borrowers from revealing the terms or even the existence of the debt.

I’m really straining my brain to understand how they thought this would play out. Did they think these debt instruments wouldn’t ever be public? This is like if a movie villian wrote the debt note. Confidentiality agreements basically prevent other creditors from accurately analyzing the financial worthiness of a debtor. It creates this perverse incentive to double pledge collateral making collection a huge, huge hassle. Which brings us to the “No Paris Club” clauses.

Lots of wonky backstory here but basically the G20 countries got together and agreed that if there were countries who defaulted on loans they would collectively restructure that debt under “G20 Common Framework for Debt Treatments”. China is saying in these contracts, “Nah, dawg, our debt has supiorirty to all that fancy pants diplomacy. Screw those Gweilos, pay us first. ” This is why these contracts need confidentiality clauses. They’ve basically declared seniority in their notes in conflict with their diplomatic obligations.

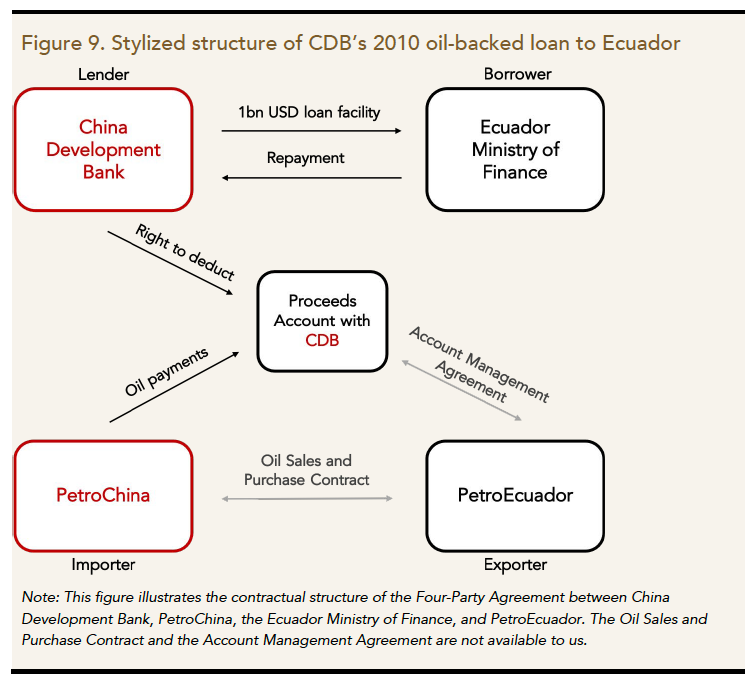

Additionally, there are some clever collateral agreements and lender-controlled revenue accounts worth talking about.

The lender-controlled revenue accounts like the above basically work like this:

China lends Ecuador money to build roads and projects and whatnot

The loan is backed by totally unrelated oil revenues

China also agrees to buy oil from Ecuador where the proceeds are deposited into a Chinese bank account

So even if the projects fail, China still get has some recourse with the Ecuadorian money in the Chinese bank accounts

I actually think this is brilliant. In practice I think a cash strapped country would find a way to redirect the oil payments but it certainly sets the bar higher for a dirtbag country to evade payment.

Lastly, there’s some fund cancellation, acceleration, and stabilization clauses worth noting:

Cross-default2 and cross-cancellation clauses trigger if the debtor takes action adverse to “any PRC entity”. The “cross” nature is less interesting to me than the broad use of “any PRC entity”. I’m going to guess that gets interpretted verrrrry broadly.

“cross-default to adverse actions that any government entity in the debtor country might take against Chinese investments there”. Again, “adverse” actions and “Chinese” investments are going to be very broadly interpreted.

"For instance, a $2 billion CDB [Chinese Development Bank] loan for the Belgrano Cargas Railway includes among its cross- cancellation triggers default or cancellation of Argentina’s $4.7 billion syndicated loan from Chinese banks to build two hydroelectric dams on the Santa Cruz River in Patagonia. CDB invoked this clause and threatened to cancel the railway project when a new government in Argentina sought to cancel dam construction on environmental grounds."

Again I think these are mostly a clever use of bargaining leverage. The cross-default clauses seem especually relevant to the US given the alphabet soup of foreign aid vehicles we tend to use.

I don’t want to downplay the whole One Belt, One Road initiative because we’re really only looking at some fraction of the debt side of things. However, these instruments strike me as more nationalistic and streamlined versions of what’s already in place from other institutions. I’m glad we have the raw data and I’ll be keen to see how these contracts get enforced.

So I’m sure there’s a bunch of One Belt, One Road stuff that isn’t lending. We’re just talking about the debt instruments in this article.

“A cross-default clause allows Creditor A to put pressure on the debtor and to protect its claim priority when the debtor defaults on its debt to Creditor B. Under a creditor-friendly version of the clause, if the debtor misses a payment to B, both A and B would have the right demand full principal and accrued interest repayment at the same time”